Related Articles

Subsidies were greatly expanded by the Biden administration during the COVID-19 pandemic as an emergency measure, but Democrats have fought to keep them permanent. Those subsidies went mostly to Democratic donors.

The 42-day federal shutdown forced by Democrats thrust the economics of Obamacare into the limelight, and exposed an uncomfortable truth: An insurance industry whose executives are increasingly liberal donors has seen its earnings soar with the injection of taxpayer-funded subsidies that propped up Barack Obama's signature health program from collapse.

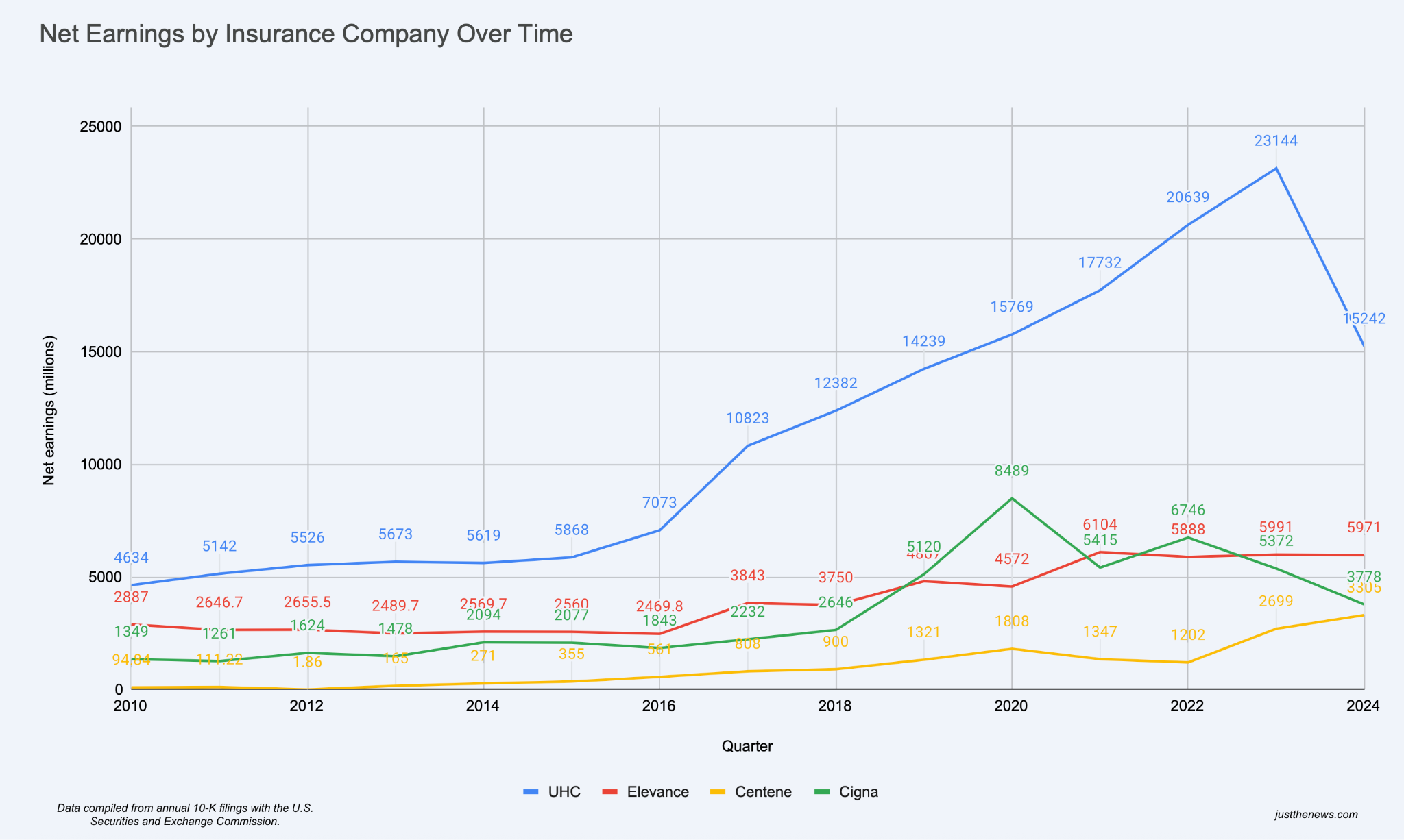

The nation’s largest health insurance companies have seen good business since Obamacare was first passed in 2010 and fully implemented in 2014. This has come in no small part because of federal government subsidies to the insurance industry, which government estimates show totaled $1.8 trillion in 2023 alone.

Those subsidies were greatly expanded by the Biden administration during the COVID-19 pandemic as an emergency measure, but Democrats have fought to keep them permanent.

A Just the News analysis of public financial records from four of the nation’s largest health insurance companies found that net earnings ballooned about 216% from 2010 to 2024. UnitedHealth Group in particular, which dominates the industry with a market share of around 15%, saw the largest explosion of profits. The other three companies, Elevance, Centene, and Cigna also experienced a marked growth in net earnings after the implementation of Obamacare.

The healthcare legislation was also a boon for these companies’ stock prices. One study found the weighted average of health insurance stock prices has grown 1,032% from 2010—when the law was passed—and 448% from 2013—the year the legislation’s key provisions were implemented.

This performance far outstripped the most popular S&P 500 exchange-traded fund, which grew 251% and 139%, respectively, the Paragon Health Institute reported last year. ETFs are designed to track the performance of specific stock indices and, as such, generally represent average market growth.

The companies’ earnings success has drawn the attention of President Trump, who on Sunday called Obamacare a scam by Democrats that benefits the health insurance industry.

“Democrats claim to be working for ‘the little guy,’ and driving down your Health Insurance, but the OBAMACARE SCAM goes STRAIGHT TO THEIR BEST FRIENDS IN THE INSURANCE INDUSTRY. THEY ARE MAKING A ‘KILLING,’ while Health Coverage only gets WORSE,” Trump posted to Truth Social.

“If Democrats get their way again, they’re in for another HUGE Payday at the expense of the American People. NO DEAL! Republicans should give money DIRECTLY to your personal HEALTH SAVINGS ACCOUNTS that I expanded in our GREAT BIG BEAUTIFUL BILL,” Trump added.

In recent years, individuals and PACs associated with these four health insurance companies have increasingly donated to Democratic presidential candidates—namely Biden and his vice president, Kamala Harris—whose administration expanded Obamacare subsidies, while contributing at much lower rates to candidate Trump.

The 2024 election illustrates this trend. Individuals associated with UnitedHealth Group contributed a total of $742,271 to Kamala Harris in the 2024 election, dwarfing the $158,000 received by the Trump campaign. Individuals associated with Centene contributed $225,622 to Harris and only $22,804 to Donald Trump. Individuals associated with Cigna sent $265,518 to Harris’ campaign compared to $99,930 to Trump’s. The only exception appears to be Elevance, which the records show did not make federal contributions in the 2024 cycle, according to OpenSecrets.

In earnings projections and investor calls, the insurance companies admit that fading subsidies would have a big impact on their bottom line. They have told their investors about plans to raise premiums on Obamacare plans and even exit markets to preserve their profit margins, showing how dependent the large companies have become on the government-backed exchanges.

UnitedHealth Group CEO Tim Noel told investors in an Oct. 28 earnings call that if his company could not negotiate “sustainable” rates, it would withdraw from markets and raise rates. He estimated that these efforts would likely result in two-thirds of its Obamacare customers dropping enrollment.

“Where we are unable to reach agreement on sustainable rates, we are enacting targeted service area reductions,” Noel told investors. “We believe these actions will establish a sustainable premium base — while likely reducing our ACA enrollment by approximately two-thirds.”

Elevance, an Indianapolis-based insurance company, also cut its 2025 earnings guidance in July after increased healthcare utilization surged costs in government-backed programs, including both ACA markets and Medicare advantage. Centene also pulled its guidance for investors, seeing market difficulty on the horizon.

The four companies did not respond to email requests for comment from Just the News.

"It is a form of corruption, it is a form of corporate welfare to very profitable insurance companies, and it has to stop," Rep. Mariannette Miller-Meeks, R-Iowa, told the Just the News, No Noise TV show on Monday.

"More importantly, it doesn't bring health care costs down. It may make it more affordable for one person, but it doesn't have any incentive for the insurance companies to bring down health care costs. So all you're doing is...that you're continuing ratcheting up premiums, because the insurance companies are getting directly subsidized by the taxpayers," she continued.

The Obamacare insurance exchanges also have another major flaw that fuels corporate profits. About a third of all subsidized Obamacare health plans go unused by the insured, meaning these plans translate into pure profits for the health insurance companies completely at the expense of the American taxpayer.

During the height of the COVID-19 pandemic, President Joe Biden signed into law a bill that enhanced the Obamacare subsidies broadly as an emergency measure, which opened the door for such over-coverage. It also raised the qualifying income cap for the tax credits to 400% of the poverty level or $128,000 for a family of four.

“These are not about the ACA subsidies, like the original Obamacare subsidies don't expire,” Rep. Dusty Johnson, R-S.D., told the John Solomon Reports podcast. “This is about the COVID-era tax credits that layer on top of that, and the tax credits don't go to Americans, they go directly to insurance companies.

He said “many people can get free policies through these pancaking layered tax credits” and some “people don’t even realize they’re double covered” because of deceptive sales tactics.

“40% of these policies have never had a single claim applied to them. It's amazing […] It shows that these are phantom policies, people aren't using them, they aren't making Americans healthier. Instead, they are just checks written to the insurance companies,” Johnson said.

This expansion “often [resulted] in federal taxpayers footing the bill for all, or nearly all, premium costs for silver and bronze plans, as well as gold plans,” the Paragon Institute concluded. Bronze, Silver, and Gold describe increasing levels of insurance plans that decrease deductible cost and lower cost sharing as you climb the rungs.

“Large insurers benefit greatly from phantom enrollment, as they collect billions of dollars in taxpayer funds to cover individuals who cost them nothing,” wrote Niklas Kleinworth, Liam Sigaud, and John Graham in a Paragon Health Institute policy brief last month.

The data show that nearly 12 million enrollees, about 35% of all people enrolled in the Obamacare exchange, are actually zero-claim enrollees. This means that their health coverage did not translate into actual health care.

Paragon found that the average profile of these enrollees is someone who is healthy and likely does not need full coverage for care. Additionally, the researchers identified worrying data that many were enrolled in full coverage without their knowledge, raising fraud concerns and leaving taxpayers to pick up the tab.

But what caused this pattern of perverse incentives? The expanded Obamacare subsidies that are now at risk due to the government shutdown, the researchers say.

“Our analysis shows that these enrollees are not just healthy enrollees with no need for care. They are part of a larger story about how Biden COVID credits are driving perverse incentives,” the Paragon authors wrote.